Bradesco: Time to Buy BBD?

B3: BBDC4, NYSE: BBD

Today we are going to talk about a Brazilian bank: Banco Bradesco S.A.

Golden years:

For many years, market leader among private banks.

It was the bank that most invested in technology in its early days.

Strong culture, training its players from the base categories.

It has already been compared to Japanese companies, due to its modus operandi.

The Downfall:

With the Itaú - Unibanco merger in 2008, it left the leadership and, little by little, began to lose its shine.

While Itaú made strategic acquisitions (XP, Avenue, …) and invested heavily in digital (Iti), Bradesco acquired (and destroyed) Ágora, which had everything to be XP Inc., bought the irrelevant BAC Florida just to say that it has a foot in the US, and tried to create 3 digital banks at the same time.

By the way, what a genius idea it is to create 3 digital banks (Next, Digio, Bitz) and stimulate competition between them, isn't it? They must have taken it from a McKinsey slide, that's for sure. What are the chances of this working?

Does anyone happen to have a friend who uses one of these Bradesco digital banks? I don't know where they get these millions of active users.

Dozens of directors earning millionaire salaries and defending the interests of their fiefdoms.

Amador Aguiar, founder of the bank, must be turning over in his grave… Poor guy.

A bank that was left without a banker. Before, Amador Aguiar. Then Lázaro Brandão. And now? You don't see a strong banker anymore.

Mammoth has aged, but not like a good Chateau Petrus.

In 3Q2022, it reported horrendous numbers after they made a mistake by lending money to those who could not pay it back. Confessed defendant.

In addition, they had a billionaire default by the Americanas retailer.

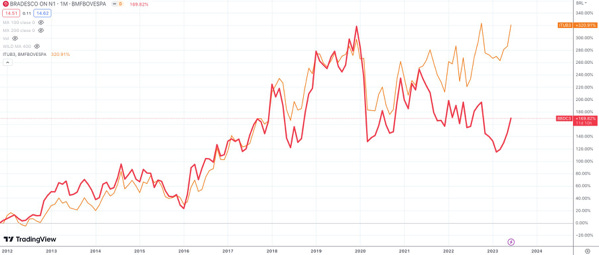

Finally, its stock, which used to go hand in hand with Itaú, seems to have lost its correlation.

Bradesco went to take a nap and it looks like he still hasn't woken up for the game.

Before x After:

Bradesco was a Rolex. Has it become a Timex?

My point of view:

There is no scenario where Bradesco regains leadership. But I believe he can be a tidy 2nd place.

His financial conglomerate model (1/3 credit, 1/3 insurance, 1/3 fees) works very well, even if it has suffered in recent years.

At some point, management will fix the credit. It's not the first time in their lives that they've had this issue. Even Itaú and Banco do Brasil have already gone through this.

Those who know Bradesco already know that it is a more cyclical bank due to the composition of the credit portfolio. So for him to go to hell and back is not expecting a miracle.

Being the 2nd largest private bank in the country, the regulator certainly has an eye on it. They won't let the business go downhill. Especially because it would be an unprecedented systemic crisis and would lead the entire economy into darkness, where Skynet would dominate the human race.

Therefore, I believe in historical mean reversion. They should fix the credit portfolio and acquire a digital bank (maybe Inter? - NASDAQ: INTR) to catch up. Thus, they will put the business on track again.

In addition, the expected drop in the Selic rate will help with operations and the expansion of the stock multiple.

Is it cheap?

Enough of the old wives' tale...

Is it to buy this stock or not?