Brazil Value Talks: Alexandre Assaf (A40 Investment Club)

Multiplied Invested Capital by 3x in 7 Years

Today I have the pleasure of interviewing Brazilian investor Alexandre Assaf.

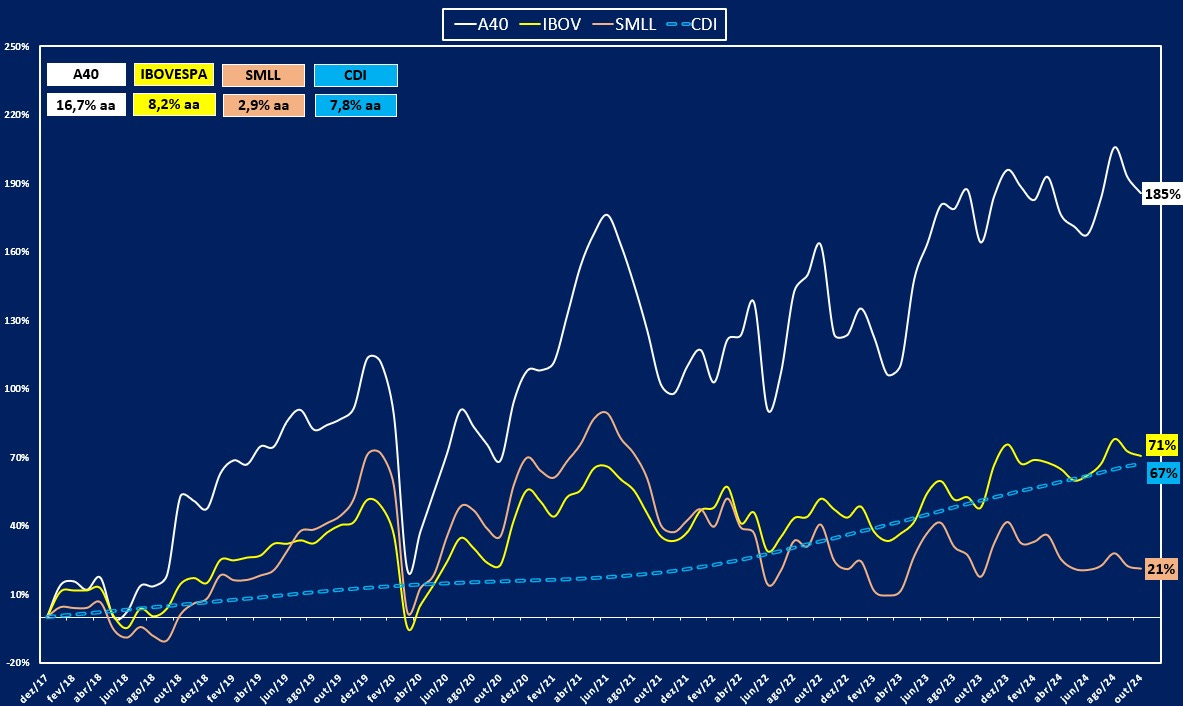

From December 2017 to October 2024 his historic performance will be the envy of anyone.

His portfolio returned more than 185% in the period, versus 71% for Ibovespa.

He multiplied the invested capital by 3x!

This guy knows how to generate real value.

Shall we meet him?

BS: Assaf, could you tell us a little about yourself?

AA: My name is Alexandre Assaf, I am from São Paulo and have a degree in Economics from the Catholic University of Santos. I am 53 years old and I am married to Adriana, an extraordinary person that God placed in my life. She gave me three children: Laura, Nicolas and Isabela. I learned from my parents that family is the basis of almost everything and I try to pass this on to them.

I have had about 30 years of experience in the business world, where I worked in an excellent company, with a unique culture and very special leaders. I had the opportunity to work in five countries and learn a lot about the areas of Finance, Planning and People.

On the other hand, I have always been passionate about the financial market. I have taken good care of the wealth that I have built throughout my life, through good asset allocation, in line with my goals and profile. Sometimes, I have invested more in stocks, and other times, more in fixed income. And I have always protected my portfolio, such as currencies and commodities. For example: I bought gold between 2021/22 (about 12% of my total assets) and it has appreciated by about 80% to date.

The good performance ended up catching the attention of some friends. Then I realized that there was an opportunity there, which encouraged me to redirect my career. I went through the entire process with CVM (this includes CFG and CGA certificates) to become a portfolio manager. In December-24, I completed the opening of the A40 Investment Club. I currently have 28 clients, with approximately R$32 million in assets under management.

I also have a future goal of donating time and money to help my wife with the social projects she is involved in. In addition to this, I believe that I can contribute to young people without access and resources in the area of Financial Education.

BS: What is your strategy for making money on the stock market?