Brazil Value Talks: Daniel Salomão

Multiplied Invested Capital by 4x in 5 Years in USD

Today I have the pleasure of interviewing Brazilian investor Daniel Salomão.

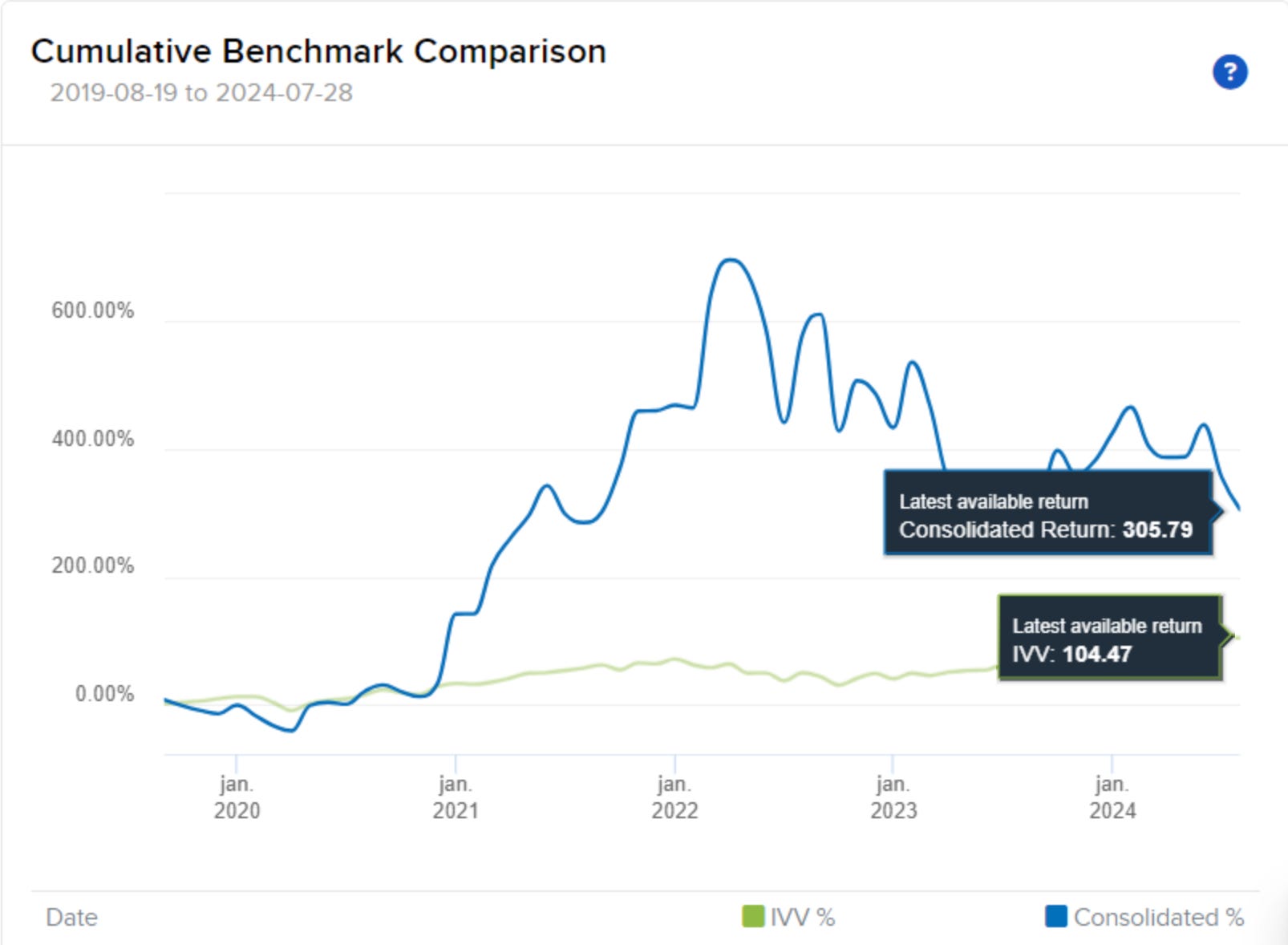

From September 2019 to July 2024 his historic performance will be the envy of anyone.

His portfolio returned more than 305.79% in the period, versus 104.47% for S&P 500.

He multiplied the invested capital by 4x!

This guy knows how to generate real value.

Shall we meet him?

BS: Daniel, could you tell us a little about yourself?

DS: I'm 43 years old and I'm from Brasília. Despite having a degree in medicine from UnB, I started studying investments at the age of 17, even before I started college. Initially, I started with fixed income, taking the interest after the implementation of the Plano Real. At 20, I started investing in the stock market.

In the beginning, the internet was still in its infancy and there were no social networks or YouTube. I also didn't know any other stock investors, so it took me a long time to learn how to deal with the market and develop my investment strategies.

Since then, I've continued studying and learning. I currently study the market and research stocks daily. And more recently, in 2019, I became a global investor, starting to invest in several stock exchanges around the world.

BS: Why did you decide to invest abroad? Isn't the competition much greater than investing in Brazil, reducing your potential return?

DS: We have raw materials abroad for whatever you want to do with a portfolio. From a portfolio that is much more stable than a Brazilian stock portfolio, with much less volatility, to totally exotic theses.

We also have a universe of small caps and microcaps that may have price distortions due to lack of coverage and liquidity. In other words, looking for more asymmetries in inefficient markets.

Another advantage is looking for sectors that are not available on our stock exchange, at least in a more artisanal way when putting together the portfolio, as was the case with uranium, for example. I have much more difficulty finding a stock that can multiply by 10x here on our stock exchange than abroad.

BS: What is your strategy for making money on the stock market?

DS: I have two boxes in my portfolio. In the first, I place stocks or cash-generating assets with lower relative risk that will build up capital in a sustained manner. In this box, I give preference to businesses that generate a good return on invested capital. Whether they will pay dividends or reinvest is a detail.

In the second box, I place stocks with convex asymmetries, that is, stocks with which I have a chance of earning a lot with a limited risk of loss. Even if one of these stocks goes to zero, the potential return is generally high: 5 to 10 times. I make estimates based on my own assumptions of probability and intensity of results. Since these are high-risk investments and often include small-cap and micro-cap stocks, I seek to mitigate risk with good diversification. The more theses and allocations, the better.

BS: What is the approximate proportion of cash-generating assets and asymmetries in your portfolio?

DS: This proportion is dynamic and will vary according to total equity. The portfolio abroad started with asymmetric theses, and I am still positioned in them. That is why I still do not have even close to the target of cash generators that I intend to have. I even have a shopping list, but not yet allocated, in several of the assets.

Since I am always finding more asymmetries, I will implement a rotation strategy based on the sales of asymmetries, with a half-and-half reallocation at first.

BS: Is it worth investing in dividend-paying stocks abroad, given that dividends are heavily taxed?

DS: Abroad, the rule is that dividends are taxed, and this requires some efficiency on the part of company managers. It is common for the overall profitability of stocks to consider share buybacks by companies, which ends up being tax efficient. So I would not focus primarily on dividends, but rather on the total value generated, with cash generation in the long term being an approximation of this, depending on the type of company.

But even for a dividend portfolio, I still think we have enough raw material to put together excellent portfolios, probably with lower total portfolio volatility than here.

BS: What is your opinion on investing in growth/tech stocks on the American stock exchange?

DS: I already had a thesis of consolidation in the sector with the big players growing more and buying or cloning everything that comes their way. In this scenario, the big players become stronger and it is increasingly difficult for an entrant to have any differentiation. Eventually, in technological or application shifts, we may have an outsider entering the playground, as was the case with OpenAI, but which is already in Microsoft's sights.

On the other hand, I am wary of buying assets that already have a premium for growth and projections built into them, in addition to the inflow due to indexes and ETFs. To solve this issue, betting on the winners is more certain with passive investments, via index ETFs, which will mitigate the risk of you not really benefiting from this growth and not having to guess the sector's movements.

BS: Do you invest in bonds of Brazilian companies in USD? If not, why not?

DS: No. First, because I have too much exposure to Brazil and, for fixed income, I prefer sovereign risk here. Another reason is that for dollarized investments, I prefer to keep the entire portfolio ex-Brazil.

BS: What is your process for finding a new buy opportunity? What filters do you use?

DS: I'm going to talk about convexities because they're less obvious. Market asymmetries don't come for free. Even though markets aren't fully efficient, they seek efficiency. If you find an asymmetry, it's usually either a high-risk stock or it's simply in what I call a 'professional blind spot'.

One of the places I like to look is in the world of abandoned and under-covered sectors or low-market capitalization stocks. I have stocks in my portfolio that were worth less than $20 million when I bought them. Investment funds and institutional investors don't usually waste time and resources searching for opportunities. I like asymmetries like this, due to lack of liquidity or reach. I don't limit myself to sectors, but I'm usually on the buying end when most people are selling stocks at a big discount.

In the natural resources sector, I took advantage of opportunities due to cyclical issues and projected imbalances between supply and demand, with my largest exposures being in copper and uranium, which I built in 2019.

When I was buying stocks in the Argentine stock market after the primaries of the penultimate elections, I was struck by the 60% drop in the stock market in dollars, the second-largest drop in a stock market in history. But obviously I did my research first, buying businesses that I thought were discounted and had very clear value anchors. For example, I bought a holding company whose net asset value in Europe and the US was worth more than the company's entire market value, with land and property assets in Argentina and other Latin American countries being priced at zero.

I also bought stocks in Russian companies after the war began, but with a very small position. SberBank is already a tenbagger (it has multiplied 10x) in my portfolio.

BS: What tools/websites do you use to search for opportunities abroad?

DS: I don't follow an index to start my analyses. As I study my theses, several others come up that I add to the list to evaluate and this list has never been empty. I started using social media platforms more recently and I like to search for asymmetries that I find on X, where I have already found several. I still don't subscribe to any portal or service abroad to help me with my theses because I haven't really needed to yet.

BS: How do you value a share: DCF, Multiples, implied IRR, a mix of the previous ones, …?

DS: For cash-generating stocks, I consider the operating cash generation capacity more, and for the company, I consider the cash-yield metric more. For asymmetries, it depends a lot on the type of stock. For example, in mining companies, I use IRR and NPV of projects or even proven reserves.

Only for property companies (real estate and land) and banks do I use book value.

I occasionally buy using simplified metrics. For example, Pampa Energia (Argentina) traded at a market value lower than one times annual EBITDA.

I recently found high-risk stocks (jurisdiction) trading at less than one times annual profit.

BS: How do you like to build your stock portfolio, considering the number of companies, sectors and concentration?

DS: I am not restricted to sectors, although I always have some property company in my portfolio.

In asymmetries, I currently have greater exposure to natural resources and mining sectors.

I prefer to diversify to mitigate non-systemic risk. Assets with low correlation, preferably negative, are ideal, but this is not essential for portfolio construction, but rather a volatility mitigation bonus.

In the asymmetry box, the more allocations, the better. However, despite having a large number of them accumulating, the size of the position follows the conviction regarding the chances of it happening or the relevance of the premium in case of success. And it may seem paradoxical, but often a very large expected premium can lead me to have a small position in the asset, especially if its risk is very high. Thus, a loss does not hurt, but success makes a difference in the overall result of the portfolio.

BS: How often do you like to rebalance your portfolio?

DS: The beauty of my two-portfolio strategy is that it reduces global volatility through cash generators and also provides potential financing in case the asymmetric fund plunges into a significant drawdown.

However, since asymmetric stocks generally do not have a very predictable time frame for success, I wait for them to move forward. If one of them generates a significant result and I sell it, part of the capital goes to the value generation fund and part is reinvested in the asymmetric theses.

BS: When do you decide to sell a stock? When it reaches its fair price or when you find an opportunity with greater potential for return?

DS: In asymmetry theses, more for the target value. In recurring income and cash generation, if the asset loses its fundamentals or if better opportunities arise, adjusted for risk, especially the ability to guarantee future cash flow.

BS: How long on average do you hold a position in your portfolio?

DS: Currently, I am accumulating more than selling, which is why I have a long average holding period of years. Naturally, cash generators do not leave unless they are replaced by better ones or because they lose their fundamentals.

As for asymmetries, I only need the theses to move forward enough for me to realize the gains, and each one has a specific exit strategy, with the rule being a staggered withdrawal until the position is zero.

BS: Do you believe that graphical analysis, together with fundamental analysis, can help with the buying and selling points of stocks?

DS: Yes, I do. But I also believe that charts reveal fundamentals sooner or later and that they serve to give us an idea of prices in relative terms.

Fundamentals always speak louder and are what motivate me to buy. If the chart is at a good entry point, even better, but it certainly is not a determining factor for buying.

BS: What are your favorite sectors on the Stock Exchange? And the ones you avoid? Why?

DS: I like the property sector because of the clarity of value measurement. I like highly cyclical sectors to look for asymmetries because they are precisely in the low phase of the cycle. I also like companies that deliver a lot of value to their stakeholders and that improve people's lives in some way.

I avoid sectors where the attempts to undertake and the capital for this are virtually infinite, but in the end they destroy value over time, such as aviation, for example. Undifferentiated retail, in a market with fierce competition. Inefficient businesses that are 'middlemen' in the market and that would be dismissed at the first opportunity.

BS: Do you use derivatives? What is your strategy?

DS: I see the main use of derivatives as hedging and portfolio protection. Occasionally, if you have little capital available, you can enter positions to catch a sharper movement in the market even with materially small allocations.

BS: What is the cheapest company on the US stock market today?