Brazil Value Talks: David Gotlib (Acertar na Mosca)

Multiplied Invested Capital by 12x versus 3x for the S&P 500 in 8 Years

I had the honor of talking to an investor with decades of experience in the market and who was one of the founders of the first hedge fund in Brazil:

David currently manages his own portfolio and is the author of the blog Acertar na Mosca, where he has been sharing his thoughts on the global economy and financial markets on a daily basis since 2011. Mosca has already accumulated more than 3,000 publications and has been consulted by more than 850,000 readers in Brazil, the United States and Europe.

From January 2016 to September 2024, his historic performance will be the envy of anyone.

His portfolio returned more than 1067.37% (USD) in the period, versus 179.53% for S&P 500.

He multiplied the invested capital by 12x!

In 2024, the accumulated performance is +24.29% in USD.

This guy knows how to generate real value.

Shall we meet him?

BS: David, could you tell us a little about yourself?

DG: I have a long career in the financial market, over 45 years. When I started, there were no microcomputers, Bloomberg, and much less cell phones or WhatsApp.

At that time, those who knew how to do math had a huge advantage, which is why banks looked for engineers.

BS: Could you tell us a little more about your academic background and how you ended up in the financial market?

DG: I graduated in Production Engineering from University of São Paulo - Brazil and, naturally, I went to work in a factory right after graduating. One day, a friend from college who worked at Banco Francês e Brasileiro told me that they were looking for engineers and asked if I would like to do an interview.

At one point in the conversation, my future boss asked: "What do you know about banks?" I was honest and said: "I don't know anything, but I'm really curious about how people make money."

I was hired and I've never left the market since; I see the market as "financial cocaine" — it's addictive and you can't stop! Hahaha...

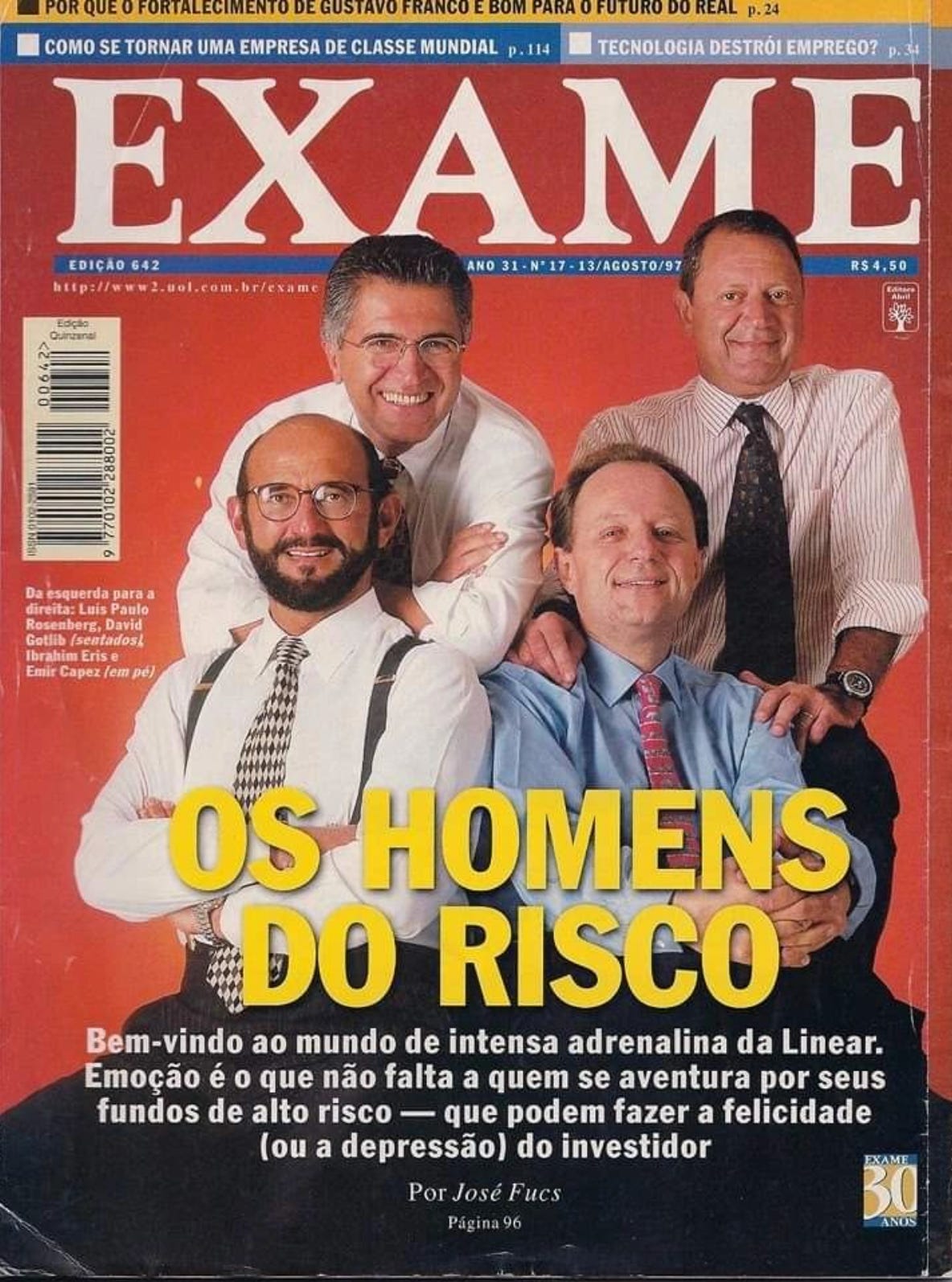

BS: What was it like to participate in the creation of the first Brazilian hedge fund in the 1990s?

DG: Linear was a startup at the time. The idea came from a trip I took to the US. Fidelity Investments inspired me to create something similar here. I already had a relationship with my former partners: Ibrahim Eris, Luis Paulo Rosenberg and Emir Capez, and I proposed that we join forces to create the first Hedge Fund in Brazil in 1993. The asset ended up having USD 1 billion under management.

After Linear, between 1999 and 2002, I was Managing Director of Deutsche Bank Asset Management, coordinating the management of funds totaling R$2.2 billion until the company was sold to Bradesco.

BS: Considering the enormous volume of currency issuance since 2008, depreciating the dollar, where should we invest to maintain purchasing power?

DG: The high volume of currency since 2008 has created numerous distortions in the markets, especially in interest rates. At this point, the dollar is always the candidate for this question. I do not have a negative view of the American currency for several reasons, the main ones being: it is still by far the main currency of exchange; and the volume of existing bonds compared to other currencies (euro, yen, etc.) still makes it a logical preference in portfolios.

I would be concerned about the dollar if there were, for example, an increase in inflation caused by a blunder (or political action) that led to an accelerated devaluation of the currency. In this case, gold would be the natural safe haven, and perhaps Bitcoin.

Regarding the latter, I am skeptical about classifying it as anything: currency, safe haven, etc. For me, they are just bits, like a perpetual bond without a coupon, which needs more and more followers every day to increase in value. For now, it serves as a "currency" for shady operations or escape in countries where the currency is in free fall.

BS: What is your strategy for making money in the financial market?