Brazil Value Talks: Pedro Henrique Dias Ferreira (Investidor SA)

Multiplied Invested Capital by 13x in 5 Years

Today I have the pleasure of interviewing Brazilian investor Pedro Henrique Dias Ferreira.

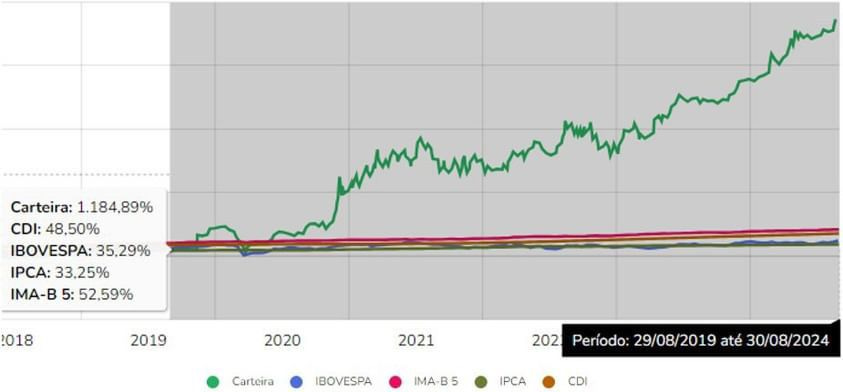

From September 2019 to August 2024 his historic performance will be the envy of anyone.

His portfolio returned more than 1184.89% in the period, versus 35.29% for Ibovespa.

He multiplied the invested capital by 13x!

This guy knows how to generate real value.

Shall we meet him?

BS: Pedro, could you tell us a little about yourself?

PF: My name is Pedro Henrique, and I have been working in the financial market since 2017 as a securities analyst (CNPI). I have worked in several areas, including investment banking, research, and asset management, and I currently work at a pension fund. I have a degree in Business Administration and an MBA in Finance.

Born and raised in Brasília, my parents always wanted me to pursue a career as a civil servant. However, my interest in entrepreneurship and the corporate world was fueled by the biographies I read, such as those of Abílio Diniz, Ozires Silva, Yvon Chouinard, and Richard Branson, among others. My decision to enter the world of finance came about when my father was dissatisfied with some investments made by the manager of the bank where he had an account. In 2013, I made my first stock purchase, and what solidified my choice for the field was a Sebrae competition, in which I was national champion in 2015. During this competition, I realized that I had an aptitude for modeling and presenting projects.

The year I started working at a bank, I created an Instagram profile, where I am quite active. Initially, the goal was to share my experiences, but over time, the profile transformed into a space dedicated to teaching and helping other investors in the stock market.

BS: What is your strategy for making money on the stock market?

PF: Although I often discuss off-the-radar theses, my portfolio adopts two main strategies. About 70% of the portfolio is focused on dividend-generating stocks, but I also include some companies that fit well as "growing companies", where I prefer to allocate resources to companies that are leaders in their markets, with a certain predictability of results and that maintain good performance even in crisis scenarios.

On the other hand, the remaining 30% is allocated to penny stocks. These are microcaps that are still in the process of gaining market share, expanding or improving their product portfolio, improving their operational efficiency and strengthening their production chains, but that present good growth potential.

I am comfortable with this division because, if a thesis about the penny stocks does not come to fruition, it will not compromise a significant portion of my invested assets.

Regarding performance attribution, 68% of the return in the period came from penny stocks, with a large weight of return coming from Taurus, a stock where I multiplied the invested capital by 8x (appreciation + dividends).

BS: What is your process for finding a new buy opportunity? What filters do you use?

PF: I prefer a more bottom-up approach, in which I focus more on the company than on the scenario, since solid companies with competitive advantages tend to have a better ability to adapt and generate returns even in adverse conditions. In addition, I focus on businesses that I understand well, such as banks and companies in the electricity sector, following Warren Buffett's advice to focus on the “circle of competence”. It is no coincidence that my oldest position is Banco do Brasil.

Regarding the 30% of the portfolio related to penny stocks, I do not follow a pre-established filter. I choose companies with a market cap below 1 billion and evaluate a series of indicators, such as economic value added. In addition, I dedicate a good deal of time to reading the minutes of the meetings, which provide valuable insights that are often overlooked by others. These minutes are an excellent source of information and serve as guidance for monitoring the company's trajectory towards its goals, including factory changes, closure of operations and integrations, for example.

BS: How do you value a share: DCF, Multiples, implied IRR, a mix of the previous ones, …?

PF: I use a combination of approaches. Multiples help with screening to identify potential assets, but they are not decisive for excluding investments. DCF, on the other hand, serves to quantify the narrative of the thesis I build about a company, and I occasionally compare my projections with the models of colleagues to assess the viability of my assumptions.

I would like to point out that in most microcaps, wearing out the soles of my shoes by visiting the company, talking to the IR department and studying the reference form to understand the business is worth more than applying filters based solely on multiples.

BS: How do you like to build your stock portfolio, considering the number of companies, sectors and concentration?

PF: I generally prefer to concentrate my portfolio. For a long time, I kept a maximum of three stocks in my portfolio, but with low correlation between them. However, as my capital increased, I felt the need to diversify my risks. Today, I own 10 stocks, but due to the still developing capital market in Brazil, the correlation between these stocks is higher than in the past.

As for limits, I never set anything in this regard. In my early years as an investor, Engie represented 100% of my allocation. With the inclusion of Banco do Brasil, I began to diversify this concentration. Currently, my largest position is one stock that represents almost 30% of my portfolio.

BS: How often do you like to rebalance your portfolio?

PF: This assessment occurs almost every six months, since most of the portfolio is rarely sold. Given the low average price of most assets, I do not increase the position until I find a safety margin that justifies the increase. I prefer to rebalance with new contributions or with funds from the liquidation of a riskier position (the so-called "little peppers").

It is important to make a disclaimer: although I maintain old positions, this does not mean that they will not be sold. Changes in the business fundamentals or in the company's direction may lead to the sale of an asset that, although it was good in the past, begins to become a potential detractor for the portfolio. An example of this was the sale of Cielo in 2019, to obtain enough capital and acquire the personal target of Taurus stocks. This change proved to be a good one, since the distributions of Taurus dividends in 2022 and 2023 were the largest I have received from a single company in a single payment.

BS: How long on average do you hold a position in your portfolio?

PF: It depends a lot on the market and also on the opportunities that arise.

The first stock I bought was Engie, buying every month and it was also the first company in which I reached R$100 thousand invested, but I sold the position in January/20, given another opportunity that arose at the time. In April/24, I bought the asset again.

BS: Do you believe that graphical analysis, together with fundamental analysis, can help with the buying and selling points of stocks?

PF: I think it's a good combination of expertise. I've even worked with some colleagues who got good results with this approach, but the most I've used in particular is Bollinger Bands and Relative Strength Index.

BS: What are your favorite sectors on the Stock Exchange? And the ones you avoid? Why?

PF: My favorite sectors are finance and public utilities, which include sanitation, electricity and gas. These sectors are what I call "anti-crisis" because, regardless of the economic scenario, people will continue to consume these services.

On the other hand, I tend to avoid cyclical sectors, such as construction and retail, since they depend on a buoyant economy to perform well.

BS: Do you use derivatives? What is your strategy?

PF: Very little and the times I used it, it was for hedging purposes.

BS: What is the cheapest company on the stock market today?