Itausa: the Brazilian Berkshire Hathaway?

B3: ITSA3, ITSA4

Today we are going to talk about a Brazilian holding company: Itausa S.A. (B3: ITSA3, ITSA4).

If you don't have an account in Brazil, you can buy shares in B3 using Interactive Brokers or ask your brokerage house to open a custody account in Brazil for you.

anuncia novo pagamento de JCP; Veja o valor")

To begin with, Itausa is not the Brazilian Berkshire Hathaway.

I'm tired of hearing this nonsense and it seems our friend below is too.

")

He deserves an apology.

They are very different companies, operating in very different economies.

Disclaimer made.

Itausa is a business holding company and its shares are among the most popular on the Brazil Stock Exchange. It's that company that the young Padawan buys at an all-time high and wants to convince you to do the same.

But does he know what he's doing?

Do I need to respond?

OK.

Who will I partner with?

Setubal and Villela families of Banco Itau.

You're already feeling like royalty, right?

I know you are.

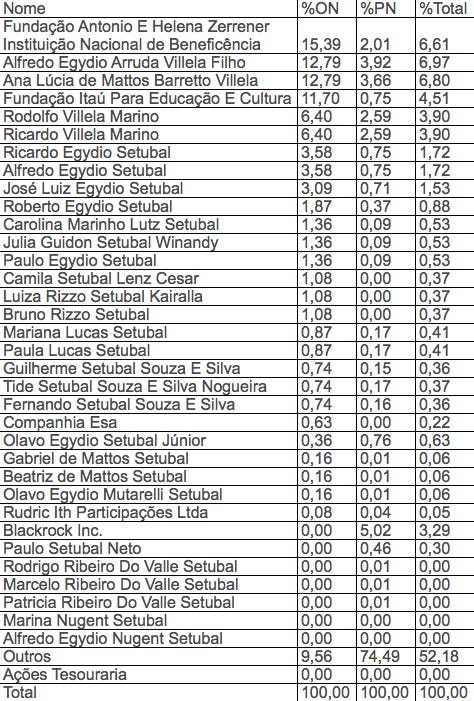

Fundação Antônio e Helena Zerrenner Instituição Nacional de Beneficência (FAHZ) is the largest individual shareholder, owning 15.39% of ordinary shares (ON).

Foundation originating from the fortune of businessman Antônio Zerrenner, founder of Cervejaria Antarctica, which later merged with Brahma, resulting in AmBev.

Its mission is to provide education and healthcare to Ambev employees and their dependents, in addition to operating in communities where the company is present.

It is the 2nd largest equity endowment in Brazil, behind Fundação Bradesco.

FAHZ holds 10.22% of AmBev shares (ABEV3), its main investment, and received R$1 billion in dividends in 2022 for this participation.

In 2017, they purchased a 15.31% stake in Itausa's ON shares from Petros (Petrobras Pension Fund) for R$4.5 billion. In 2022, its participation yielded R$300 million in dividends.

Despite FAHZ's shareholding position, there is a Shareholders Agreement between the Setúbal and Villela families, representing 63% of ON. In this way, this Control Block is the one who commands the company.

What is Itausa?

It is a holding company formed 90% by Banco Itau and 10% by various minority interests in other companies.

After 30 years investing mainly in the financial sector, until it was consolidated, 10 years ago Itausa began to diversify, allocating its capital in non-financial sectors.

The focus defined in recent years is to invest in good dividend-paying companies, as if it were a dividend portfolio.

Itausa's Dividend Policy is to fully pass on dividends received from Itau.

Itausa's businesses are:

Banco Itau (39% of ONs). No introduction required. It is the largest financial conglomerate in the Southern Hemisphere. It represents 90% of Itausa's revenue and is where the dividends it distributes come from. It grows little, in line with inflation.

Alpargatas (44% of ON, 15% of PN, 29% of the Total). Considered a favorite for many years, in 2017 Itausa purchased J&F's stake from the Batista brothers. Alpargatas is not a good dividend payer as it trades at high multiples. Since 2016, it has been unable to grow any further, and perhaps because of this, to justify its valuation as a growth company, it has started making acquisitions. Each acquisition, a new tragedy, a drain on money. Alpargatas generally performed very well under Marcio Utsch's management (2003-2019). The CEO and CFO were recently changed after the company experienced operational problems. An ex-AmBev was called to try to bring order to the house. Itausa is a partner of the Moreira Salles do Itau family in this business.

NTS (8.5% of ON). It is a network of gas pipelines that Petrobras sold to a consortium led by Brookfield and which included CIC funds, from China; GIC, from Singapore; and British Columbia, from Canada. The consortium owns 91.5% of the company, and Itausa, 8.5%. NTS transports half of all natural gas in Brazil.

Aegea (10% of ON, 19% of PN, 13% of the Total). Controlled by the construction company Equipav, with 70% of ON shares, and with GIC also being an investor in the company, Aegea is the leader in private sanitation in Brazil. They recently won the auction to operate sanitation in some parts of Rio de Janeiro (CEDAE) and also CORSAN (RS). Although personally I don't really like being a partner in a construction company, it is a good dividend-paying business and has a lot of potential for growth. They intend to do an IPO at the next opportunity that arises.

CCR (10% of ON): CCR operates relevant concessions for highways, airports and subways that connect all corners of the country. Together with Votorantim, they purchased Andrade Gutierrez's share in the company. They are now partners with Soares Penido and Camargo Corrêa. I actually like the road concession business, the problem is being a partner with large construction companies. They put in a very good CEO, the one who put Log-In (LOGN3) back on track, but he left the company after 1 year in office. I don't have a good feeling. It is a good dividend payer, but is going through a bad time.

Dexco (40% of ON). They are partners of the Seibel family (20%) in this business, which was previously called Duratex. It is the largest company producing industrialized wood panels in Brazil, the market leader in the production of sanitary ware and metal fittings in the Southern Hemisphere and one of the leaders in the ceramic tile segment in the country. It is a cyclical business and, therefore, is not an excellent dividend payer. Itausa has been a shareholder for many years.

Copa Energia (49% of ON). Members of the founding family, Zahran. It supplies liquefied petroleum gas (LPG) and intends to enter renewable energy. Privately held company that will probably do an IPO at some point.

XP Inc. (6.6% of ON). Itau bought a stake in XP and wanted to buy more. The idea was to reach 100% participation, but the Central Bank vetoed it, so Itau distributed XP shares to its shareholders. In this way, Itausa received shares in XP, which it is selling little by little. Itau's plan is to copy everything that XP has to offer. It is not a good dividend payer and the competition is attacking hard.

My Point of View:

FAHZ buying 15.39% of Itausa, for me, is the biggest sign of what Itausa is: a good dividend payer.

Alpargatas was a good business. It seems that in recent years it has become a bomb, but this only represents ~2% of the total, so there is no need to worry.

Dexco doesn't have that dividend profile, but I don't see a problem with it, and it's also a small holding.

The remaining positions, except XP, which is being sold, are maturing and have the potential to pay good dividends in 3-4 years.

Over time, Itau's share in Itausa's consolidated portfolio will fall, but this is a gradual movement and will take many years to really have an important effect.

Diworsification: there is a risk that these new investments will not produce the same return as Itau, so the holding company's return may gradually be compressed.

For the next 5 years, buying Itausa will still be the good old buying Itau with a 20% discount. This way, you receive a "1%" higher dividend yield than if you bought Itau.

Carrying this action for the long term, I estimate a return of 12% p.a. It's not bad, but it's not excellent either.

But, if you know the right point to enter and leave it, then the return can be explosive.

Is it cheap?

After all, is it to buy this stock or not?

What is the price to buy and sell ITSA4 after all?

I'll show you all the rationale, in detail.

Let's go.